In 2025, the question of is Karma credit correct has become increasingly relevant for many users. More individuals rely on free services to track their financial health.

So, it is crucial to understand the accuracy of tools like Credit Karma. People seek clarity on how precise their credit information is and how it impacts their financial decisions.

Overview of Credit Karma’s Accuracy

This article offers an in-depth analysis of the accuracy and reliability of Credit Karma while exploring its features and alternatives. Many users wonder, is Karma credit precise? Understanding this can help users make informed decisions about their financial health.

Real User Testimonials

Before diving into the specifics, here are insights from actual Credit Karma users:

- John D.: “Using Credit Karma has been a game-changer for me. I check my score regularly and appreciate how easy it is to understand.”

- Lisa M.: “I love the insights Credit Karma provides. Nevertheless, sometimes I wonder how precise the information is compared to what lenders see.”

The Short Answer

Credit Karma is generally precise but does not show your FICO score. Instead, it utilizes VantageScore 3.0, relying on data from TransUnion and Equifax. While these scores are legitimate, they vary from what lenders see when assessing your creditworthiness. Thus, the question, is Karma credit correct? can often lean towards the positive, but it requires context.

Key Findings: Credit Karma Accuracy

- Scoring Model: Uses VantageScore 3.0 instead of the FICO scoring model.

- Bureau Coverage: Reports from two (TransUnion and Equifax) out of three major credit bureaus.

- Frequency of Updates: Scores are updated weekly.

- Free Services: Provides credit monitoring at no cost.

- Trust Rating: Maintains an A+ BBB rating.

How Credit Karma Works

Credit Karma collects data directly from TransUnion and Equifax. The service operates using VantageScore 3.0, which is developed by the three main credit bureaus. To understand Credit Karma accuracy, you need to identify why differences arise. These differences occur between Credit Karma scores and those from other sources.

Reasons for Score Discrepancies

- Different Scoring Models

- VantageScore 3.0 is used by Credit Karma.

- Lenders typically rely on FICO scores.

- Each model weighs credit factors differently.

- Limited Bureau Data

- Credit Karma does not include Experian data.

- This absence overlooks significant credit changes.

- Timing of Updates

- Credit Karma updates scores weekly.

- Lenders view more recent information.

- Credit reports can update at varying times.

Pros and Cons of Using Credit Karma

Pros

- Free Credit Monitoring: No cost involved.

- User-Friendly Interface: Easy navigation.

- Weekly Updates: Keeping information fresh.

- Educational Resources Available: Helps users understand their credit.

- Identity Theft Monitoring: Protection against fraud.

Cons

- Lack of FICO Scores: Not presenting a critical scoring model.

- Limited Data Coverage: Missing Experian information can affect holistic understanding.

- Ad-Supported: Some users find this unappealing.

Expert Recommendations

Financial experts advocate for utilizing Credit Karma alongside other tools for monitoring credit. While it is particularly useful for tracking trends, it should not be the sole source of credit information.

Best Practices for Credit Monitoring

- Check your FICO scores annually.

- Review reports from all three major credit bureaus.

- Use Credit Karma for regular casual monitoring.

- Understand the differences between scoring models.

- Concentrate on credit score ranges rather than specific figures.

Comparative Analysis with Other Credit Monitoring Services

When comparing is Karma credit precise to other credit monitoring services, consider:

- Service Coverage: For example, services like Experian offer access to all three major bureaus.

- Scoring Models Used: Credit Sesame uses VantageScore but also offers limited FICO scoring options.

- Cost of Services: Compare free services like Credit Karma. Then consider subscription models like Identity Guard. These models are known for comprehensive identity theft protection.

- Extra Features: Many services offer extra benefits, like tax filing assistance or budgeting tools.

Credit Karma Features

Credit Karma offers a range of features that draw users, including:

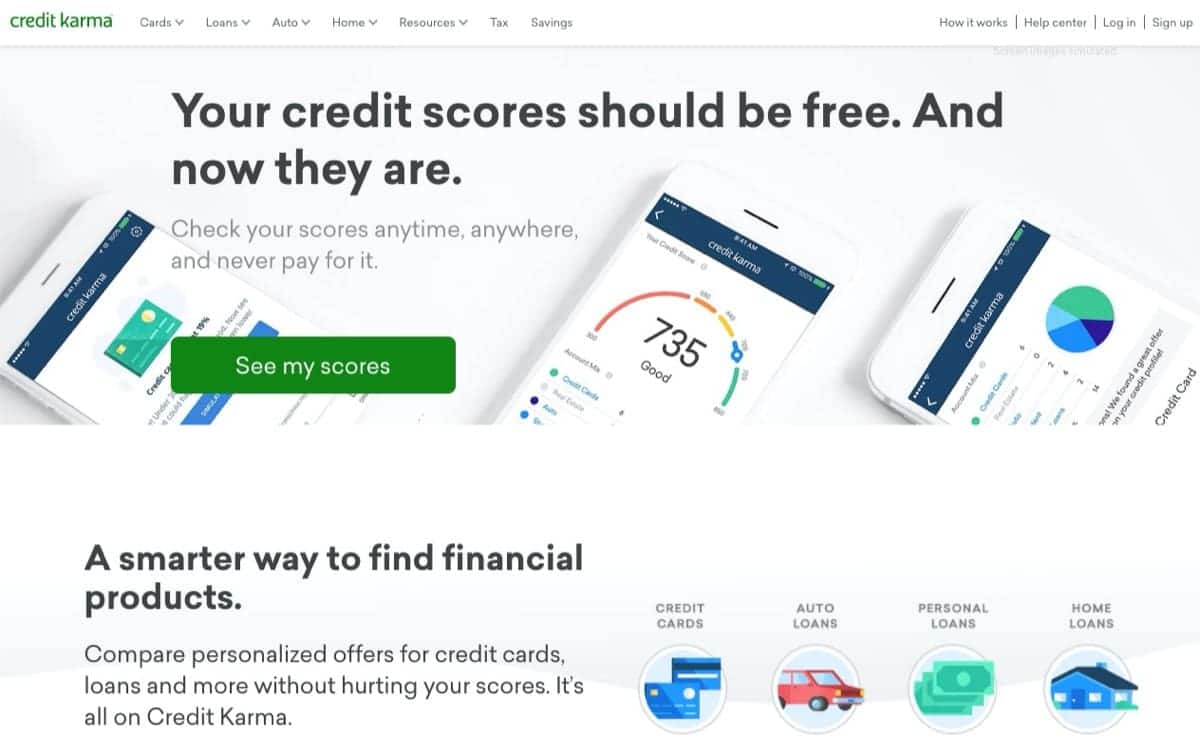

Free Credit Scores

Credit Karma’s main feature is providing free credit scores from both TransUnion and Equifax. You get these scores when you sign up for a free account. You can click on the scores to see more details, including payment history, credit utilization, and length of credit history.

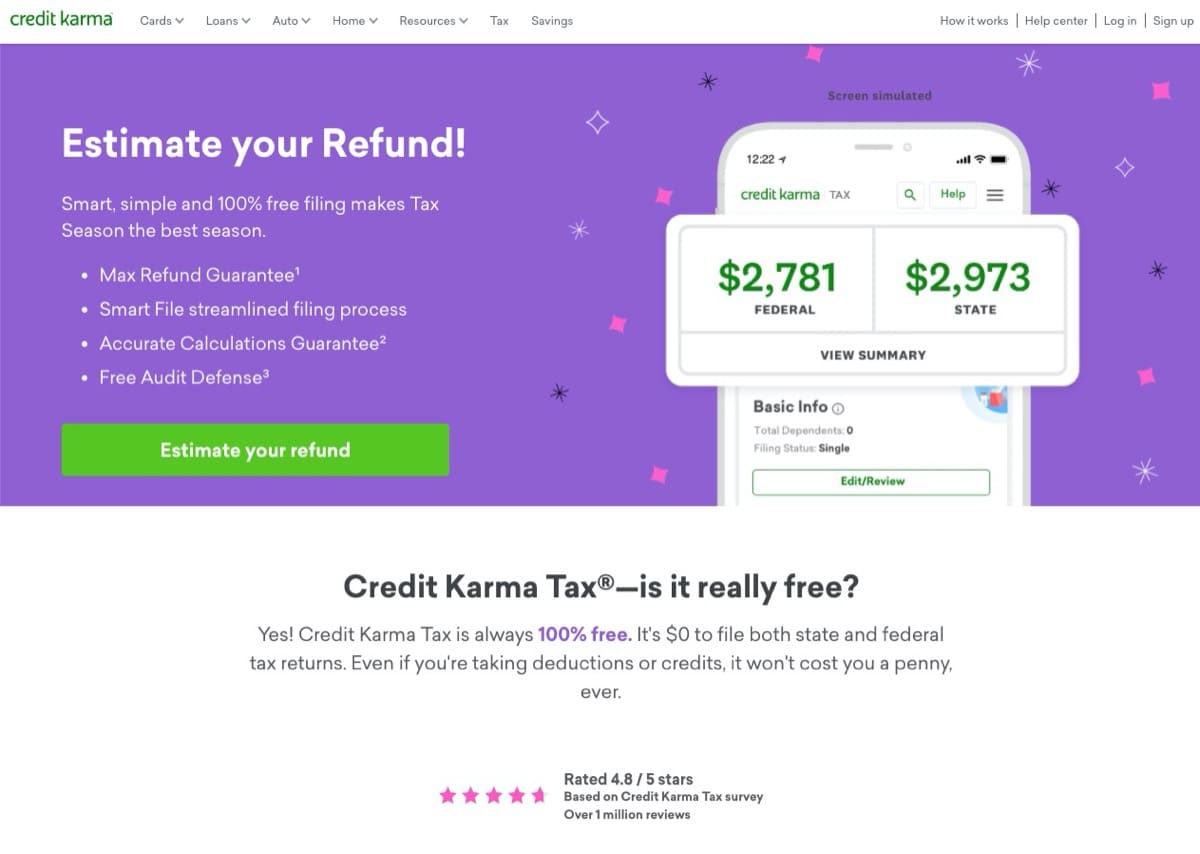

Credit Karma Tax

Credit Karma Tax is a free service that allows users to file federal and state taxes. It offers features like Smart File, Audit Defense, and a Max Refund Guarantee.

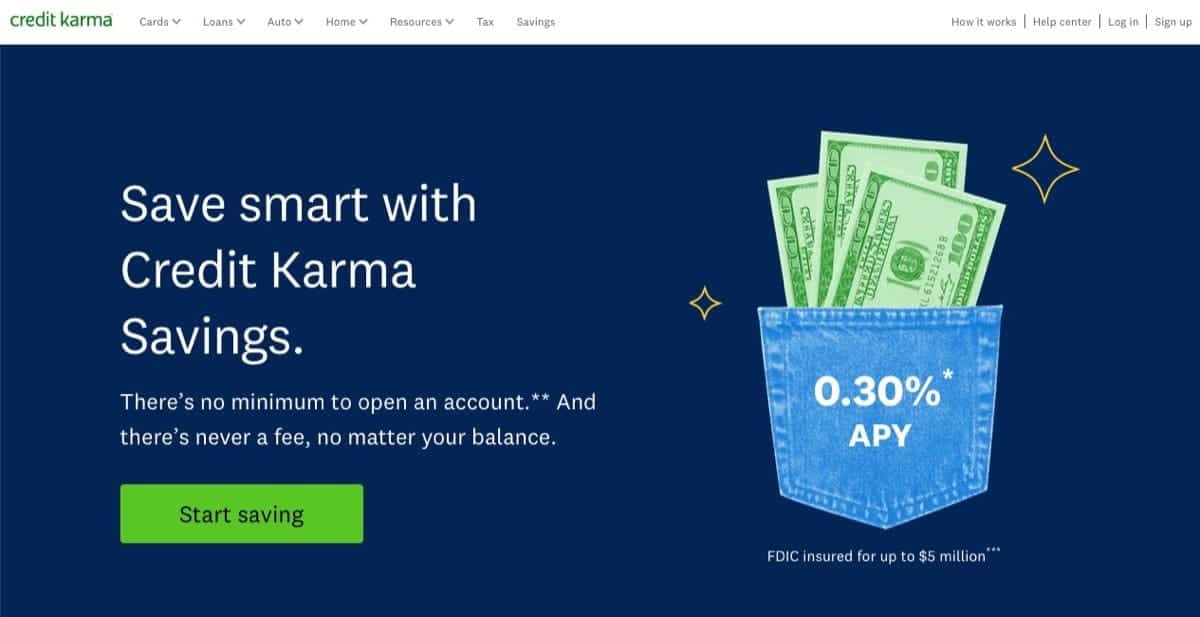

Credit Karma Savings

Credit Karma Savings features high-interest savings accounts without fees or smallest balance requirements, making it a competitive choice.

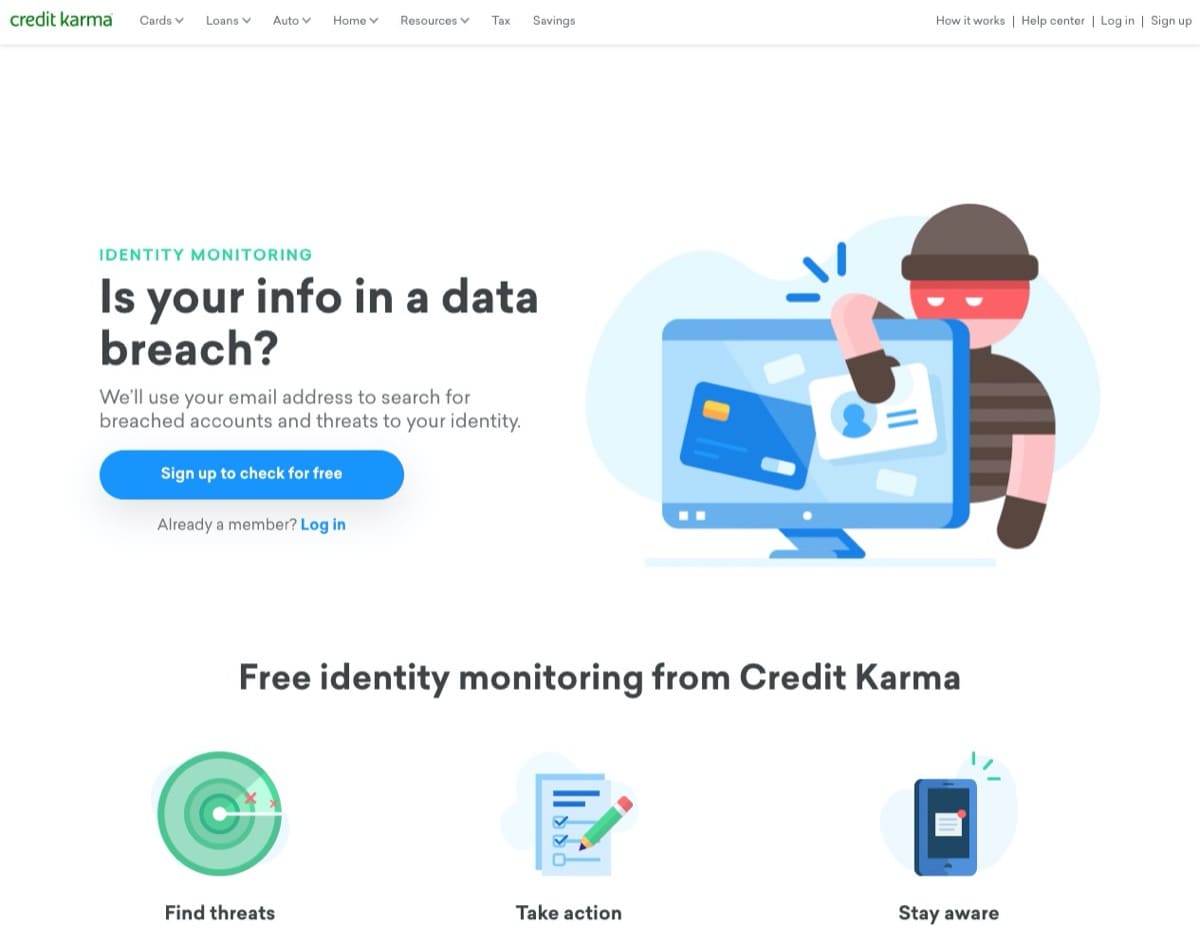

Identity Monitoring

Credit Karma’s identity monitoring alerts users about compromised accounts and scans the dark web for personal information.

Unclaimed Money Search

Users can search for over $40 billion in unclaimed money from state governments. This can be done via Credit Karma accounts. The platform simplifies the claim process.

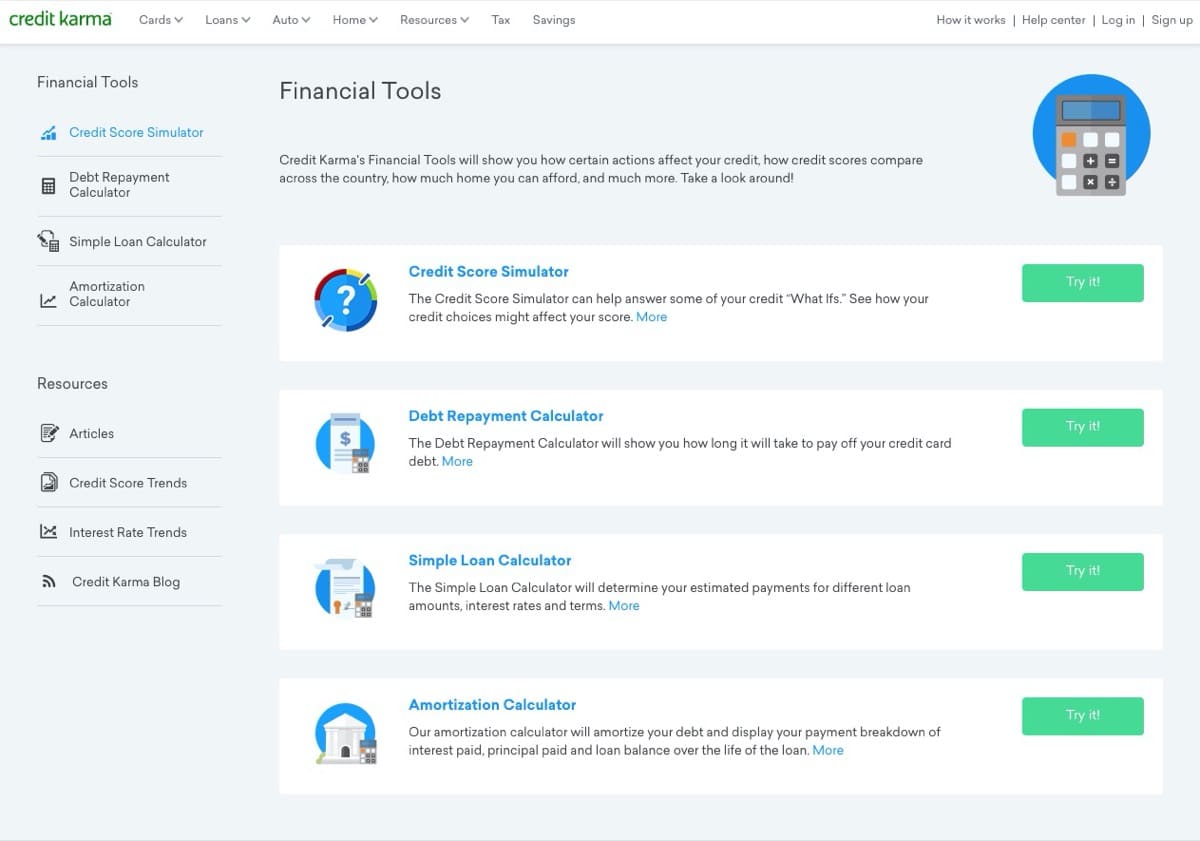

Financial Calculators

Credit Karma offers financial calculators. One example is the Credit Score Simulator. These tools help users understand how their actions affect their credit scores.

How Does Credit Karma Make Money?

Credit Karma makes money through affiliate marketing. They recommend products and get compensation from banks or lenders. This occurs when these recommendations are used.

Conclusion

Credit Karma offers a free credit score estimate, aiding users in tracking their credit health. Yet, it’s crucial to remember that it does not give the exact scores used by lenders. Users should complement Credit Karma with other tools for a holistic understanding of their credit standing.

Over 100 million Americans use it for easy access to credit scores and reports. Signing up only takes 3–5 minutes.

Interested in managing your credit score better?

Explore our detailed guide on effective credit monitoring tools and strategies to safeguard and enhance your financial standing.

Get started with Credit Karma

Getting started with Credit Karma is safe and completely free. You can use Credit Karma by downloading the mobile app from the App Store. Alternatively, download it from Google Play. You can also sign up on their website.

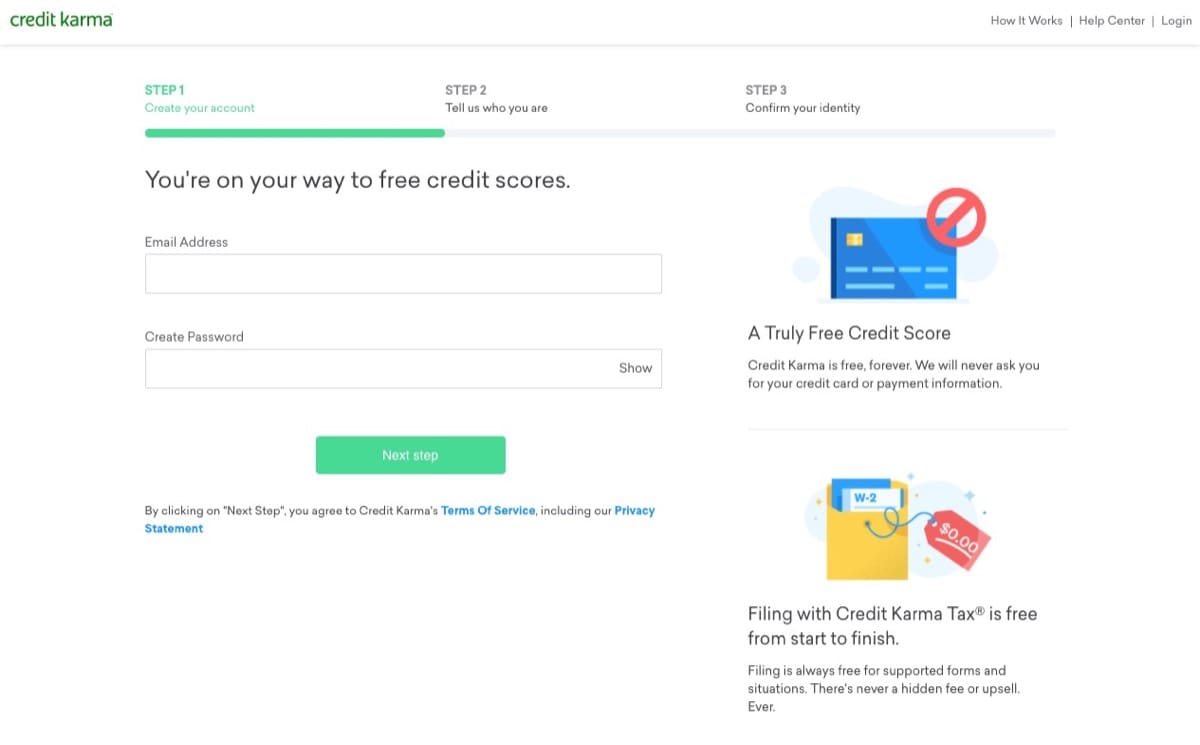

Create your free account

Step 1: On the homepage, look for a button that says See my scores or Get started. Click on either button to start creating your account.

Step 2: Enter your email address and password, then click the Next step button.

You will need to give personal information. This includes your full name and location. You will also need to give your date of birth and the last four digits of your Social Security Number.

Providing your SSN’s last four digits helps Credit Karma access your credit scores and reports. It does not harm your credit score.

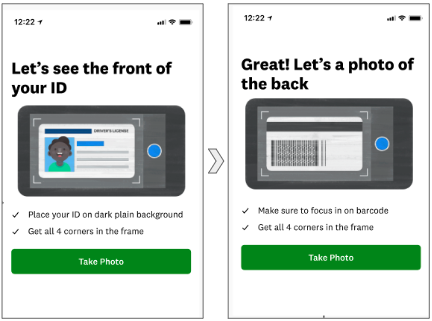

Step 3: Verify your identity with documentation like a government-issued photo ID and proof of residence.

People Also Read

- Save More with Financial Resources and Tools

- 4 Tips for Young Adults to Avoid Long-Term Debt

- Refund and Returns Policy

- Places to Eat Free When You Post About Your Meal

If you find any inaccuracies on your credit report, you can dispute the error using Credit Karma. For more details, visit consumerfinance.gov/owning-a-home/prepare/check-your-credit.

Leave a Reply